All Assets Today Are Backed by the Treasury Bond

Leave a reply

Mario Draghi today promised to do whatever it takes to fix the euro. ”Believe me, it will be enough.” I don’t know why anyone would believe him, but that is not the point of this article.

There is a Monetarist premise that is accepted almost universally today: the value of a unit of currency is inversely proportional to the money supply. If the money supply goes up, this view argues that the value of the currency must go down. And vice versa. There is only one problem with this idea.

It is wrong.

The euro has been falling against the US dollar for over a year and the most recent leg down began in earnest in May. It has not been falling due to expanding money supply. It has been falling due to increasing market awareness that defaults are coming–reflected in collapsing bond prices not only in Greece but in Spain and Italy now.

And this brings us to Draghi’s statement today. He was not promising to decrease the money supply! All of the “tools” in his “arsenal” are tools to increase the money supply. Basically, he can print and lend (i.e. print money and lend it).

Today, he reiterated his means and intent to expand the money supply. And the euro went up +1.6%.

Something to make one go think in the night …

This paper is published here.

By now, most readers are aware that Barclays and probably many other banks have been caught red-handed gaming the London Inter-Bank Offer Rate (LIBOR).

No, I am not going to analyze the “cause”, call for more regulation, propose lawsuits, or lament that “banksters” today are “greedy”. I have a simpler and subtler point.

In the regime of irredeemable paper money, the interest rate is always a manipulation!

The very purpose of a central bank is to be the “bidder of last resort” (on the bond), which means to drive down the rate of interest. A quick look at the rate of interest on the 10-year Treasury bond shows that they have been succeeding for the last 31 years.

What difference does it make whether a thief at the government / central bank robs the saver of his savings, or whether a liar at a nominally private bank robs the saver of his savings? Why is the former considered legitimate? If the latter does it, why do people demand to give more power to the government to “regulate” the nominally private banks?

The fact is that under irredeemable paper, the saver cannot get a yield worthy of his time commitment, much less risk. Governments and central banks have deliberately pursued a policy of trying to “stimulate” demand by creating artificial disincentives to saving. If you have cash, the government wants to push you to either spend it or invest it in risky assets.

Instead of jerking our knees at the LIBOR manipulation, isn’t it time that we started to demand a repeal of the legal tender laws and taxes on the “gains” of gold and silver? These are the primary means by which savers and creditors are forced to use the Fed’s paper scrip. Without these bad laws, savers would be re-enfranchised and a whole host of changes would occur in the monetary system. It would be about time.

I gave two lectures on Irredeemable Currency vs. Gold.

In Session 1, I discuss the intractable problems.

In Session 2, I discuss the proper system and a solution how we can transition to it.

Today, short-term interest rates are set by the diktats of the central bank. And long-term interest rates are set in a “market” in which the central bank is obliged to keep coming back to buy ever more bonds, and speculators front-run the central banks to buy ahead of them. The result has been that, for 30 years and counting, the bond price has been rising, which is the same as to say that the rate of interest has been spiraling into the black hole of zero. When it gets there (and probably sooner) the entire monetary system will collapse.

This is the terminal stage of the disease of irredeemable paper currency. They have banished money (gold) from the monetary system, and the result is a positive-feedback-loop that destabilizes the rate of interest. The rate of interest has a propensity to fall, just like the value of the paper currency itself.

This leads to the question of how interest rates are set by a free market under a gold standard. This is a non-trivial question, and the answer is profoundly important as we debate what sort of role gold ought to play and evaluate the various gold standards being proposed.

If people are free to own gold coins directly, then the mechanics of setting the rate of interest are simple. Let’s define a term. The marginal saver is the saver who could go either way, either holding a bond or a gold coin. If the rate of interest ticks downward, he will sell the bond (or withdraw his money from the bank, thus forcing the bank to sell the bond) and buy the gold coin. He would rather hold the gold than commit to the time and risk for such a low interest rate. If the rate of interest ticks upward, he will buy the bond (or deposit his coin in the bank).

The marginal saver sets the floor under the rate of interest. It cannot fall below his preference or else he will vote with his gold. His preference has real teeth (unlike today).

Now let’s define one more term. The marginal entrepreneur is the entrepreneur whose rate of profit is the lowest possible, while still being viable. If his profit falls for any reason, such as due to a rise in costs, he will shut down his enterprise. One cost is the cost of capital, i.e. the rate of interest. No entrepreneur can borrow at a rate higher than his rate of profit, and the marginal entrepreneur is the first to buy the bond and sell his capital stock at an uptick in the rate of interest. He is the first to sell a bond and buy capital stock at a downtick in the rate.

The marginal entrepreneur sets the ceiling over the rate of interest. It cannot rise above his ability to pay, or else he will vote with his capital stock. He also has teeth.

Under a proper gold standard, the rate of interest is kept in a band that is not only narrow, but which is also stable over long periods of time. This is the principle virtue of the gold standard. It does not fix the level of prices, which would be neither possible nor desirable. It keeps the rate of interest consistent, which serves the interests of wage earners, pensioners, and other savers, and of entrepreneurs whose work provides the goods, services, jobs, and interest payments that on which everyone else depends (and which they take for granted).

When evaluating any proposed gold standard, one should ask the question: how will it determine the rate of interest?

Recently, I gave two lectures in Phoenix on this topic. In the first lecture (links below), I present the problem. Hint: bankruptcy.

In the second lecture (will be posted online soon), I present my proposed solution.

Irredeemable Currency Session 1, 1/2

Irredeemable Currency Session 1, 2/2

The current financial crisis, may progress to a phase where people demand and hoard dollar bills but take electronic deposit credits only at a discount which increases until electronic deposit credits are repudiated entirely. The Federal Reserve would be powerless to solve the problem, because while they can create unlimited electronic deposit credits they can’t create unlimited paper dollar bills, “money you can fold” as Professor Antal Fekete calls it. There would be a glut of electronic deposits, but a shortage of dollar bills.

Before the financial crisis metastasized in 2008, Fekete wrote a paper that I think is underappreciated and under-discussed. Can We Have Inflation and Deflation at the Same Time? In his paper, he discussed the “tectonic rift” between paper Federal Reserve Notes (i.e. dollar bills) and electronic deposits. By statute, the Federal Reserve cannot print dollar bills without collateral (e.g. Treasury bonds). Also, they have limited printing press capacity that is insufficient to keep up with a catastrophic crisis.

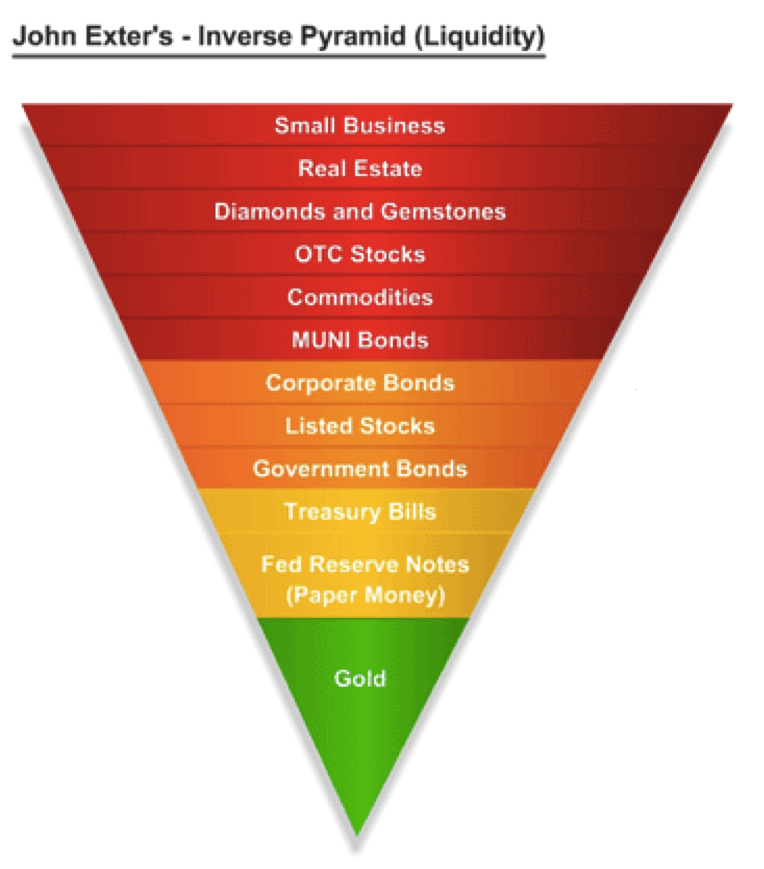

He discussed the inverted pyramid of John Exter. Gold is the triangle at the bottom, and then above is silver, dollar bills, and then the various kinds of electronic deposits, stocks, real estate, etc. In a crisis, people want to move from top to bottom of the pyramid, but of course there isn’t enough of the stuff at the bottom.

In a scenario in which desperate, panicky people are trying to cope with the enormity of a collapse that they don’t and can’t understand, I think this split between “physical” dollars and “electronic” dollars is very plausible.

Just as there is nothing to be accomplished by selling an underlying security as it becomes worthless, only to buy a derivative of it, selling Treasury bonds and buying dollars is equally nonsensical. The dollar is the Federal Reserve’s liability, backed by the Treasury bond as the asset. If you believe the Treasury bond is worthless, then you ascribe no value to the dollar either. This is why gold will go into permanent backwardation. Holders of dollars will provide an unlimited bid for gold that will not be reciprocated by holders of gold. The latter own the only safe asset, and the only monetary asset that is not ultimately backed by the Treasury bond or the dollar, and they will have no desire to give it up.

The concept of backwardation is simple. It is when people accept a future promise to deliver only at a discount to physical stuff handed over right now. This could be when there is a shortage, such as wheat before the harvest. Or in the case of gold, backwardation signifies a collapse in trust. But isn’t this the same phenomenon of a tectonic rift between paper dollars and electronic deposits?

In a certain sense, the “money you can fold” behaves like a physical commodity, a present good (I realize I am stretching the concept here more than a bit). The electronic deposit credit is most definitely a future promise. In my gold backwardation thesis, the action begins with the offer on the futures contract falling below the bid on spot gold. The bid-ask spread on spot gold widens, as the offer is relentlessly advancing, pulling the bid behind it. The bid-ask spread on the futures contract also widens, as the offer remains stubbornly high, but the bid withdraws and retreats as gold buyers don’t trust futures and buy physical gold instead. Eventually, there are no more sellers of physical gold and that is that (except for the dollar-commodities-gold arbitrage, a backdoor way for dollar holders to get a little gold before the end of the game).

If this split occurs in the dollar, I think it will play out the same way. At first, sellers of real goods may accept electronic credit money, but demand a higher price. The spread on the electronic dollar widens, with the bid from real goods falling. At the same time, virtually unlimited demand for the “real” paper you can fold causes the bid on the paper dollar to rise.

Who knows how long it could last? People could go on accepting paper dollars out of long habit. Obviously, this is an unstable situation that must necessarily collapse. Unlike gold, the paper dollar has no value other than the broken promises that back it.

I dub this “dollar backwardation”.