A recurring theme of mine is that one cannot understand the world in terms of the linear Quantity Theory of Money. Let’s look at the cost of shipping.

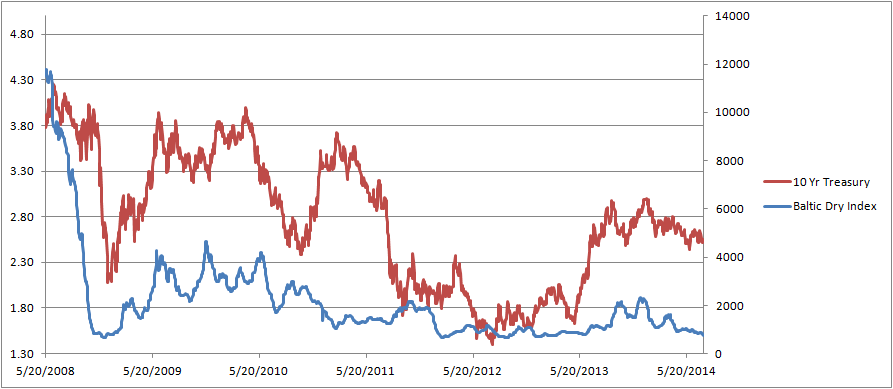

The money supply has certainly been expanding since 2008. And yet the price of shipping has almost completely collapsed. From a high over 11,000 it’s now down to 755. This is a drop of almost 94%.

The Baltic Dry Index is a dollar price of moving the major materials by sea. The chart shows from just before the acute phase of the crisis to today, July 16, 2014.

I like to look at the Baltic Dry because, unlike commodities, there is no way to speculate on it and hence drive up the price. (If readers are aware of some sort of futures market or other way for speculators to use credit to bid up prices, then I encourage them to please contact me.)

Neither the money supply nor supply and demand adequately explains this collapse. Supply and demand may be a tempting model, but it raises more questions than it answers. Is it falling demand or rising supply? Why would supply rise so much? Why would demand collapse? Could both be occurring at the same time, and if so are the business managers and their bankers that blind?

The Austrian Business Cycle Theory is a much better way of thinking about this.

Ultimately, this graph tells a story of credit expansion and credit contraction. During the expansion there was lots of demand for shipping. Naturally this led to malinvestment in ships. During the contraction, the ships aren’t needed but they cannot be unmade. More importantly, the money borrowed to finance them cannot be unborrowed.

Why was there so much malinvestment? The rate of interest has been falling during this time (and much longer). The lower the rate, the more attractive it is to borrow to buy a capital good, such as a bigger ship. On this graph, the interest rate on the 10-year US Treasury bond is added. The correlation isn’t perfect by any means, but there is something here.

It is important to realize that a company that borrows to malinvest sees a profit at the time. That’s what so deadly about central planning of money and credit. The central planners push down the interest rate, and this sends a false signal. The shipping companies and financing companies calculate the profit in building new ships. They are neither stupid nor incompetent.

They may not lose money at all. The losses may go to some existing shippers, particularly those who previously built ships, with money borrowed at higher interest rates.

No matter who it is, we can be certain that somewhere in the world, there are debtors being put to the squeeze. And with equal certainty, we can say that their lenders—including banks—have assets on their balance sheet that will need to be written down (or written off).

And when that happens, it adds to the bust. Desperate lenders sell assets onto whatever bid they can find. Asset prices begin to plunge. Arbitrages connect those assets to other assets, not to mention margin calls. Workers lose their jobs, investors lose their money, and businesses close.

The dollar, with its interest rate dictated by the monetary politburo, is destroying people’s lives. One important virtue of the gold standard is that it has a stable interest rate, set by the participants in a free market. It worked and it will work again when we finally reject the regime of irredeemable paper money.