In Part I, we looked at the concepts of nonlinearity, dynamics, multivariate, state, and contiguity. We showed that whatever the relationship may be between prices and the money supply in irredeemable paper currency, it is not a simple matter of rising money supply –> rising prices.

In Part II, we discussed the mechanics of the formation of the bid price and ask price, the concepts of stocks and flows, and the central concept of arbitrage. We showed how arbitrage is the key to the money supply in the gold standard; miners add to the aboveground stocks of gold when the cost of producing an ounce of gold is less than the value of one ounce.

In this third part, we look at how credit comes into existence (via arbitrage, of course) with legitimate entrepreneur borrowers. We also look at the counterfeit credit of the central banks (which is not arbitrage). We introduce the concept of speculation in markets for government promises, compared to legitimate trading of commodities. We also discuss the prerequisite concepts. Marginal time preference and marginal productivity are absolutely essential to the theory of interest and prices. That leads to the last new concept resonance.

In the gold standard, credit comes into existence when one party lends and another borrows. The lender is a saver who prefers earning interest to hoarding his gold. The borrower is an arbitrager who sees an opportunity to earn a net profit greater than the rate of interest.

As with all markets, there is a bid and an offer (also called the “ask”) in the bond market. The bid and the offer are placed by the saver and the entrepreneur, respectively. The saver prefers a higher rate of interest, which means a lower bond price (price and interest rate vary inversely). The entrepreneur prefers a lower rate and a higher bond price.

Increased savings tends to cause the interest rate to fall, whereas increased entrepreneurial activity tends to cause a rise. These are not symmetrical, however. If savings fall, then the interest rate must go up. The mechanism that denies credit to the marginal entrepreneur is the lower bond price. But, if savings rise, interest does not necessarily go down much. Entrepreneurs can issue more bonds. Savings is always finite, but the potential supply of bonds is unlimited.

What is the bond seller—the entrepreneur—doing with the money raised by selling the bond? He is buying real estate, buildings, plant, equipment, trucks, etc. He is producing something that will make a profit that, net of all costs, is greater than the interest he must pay. He is doing arbitrage between the rate of interest and the rate of profit.

It may seem an odd way to think of it, but consider the entrepreneur to be long the interest rate and short the profit rate. Looking from this perspective will help illustrate the principle that arbitrage always has the effect of compressing the spread. The arbitrager lifts the offer on his long leg and presses the bid on his short leg. The entrepreneur is elevating the rate of interest and depressing the rate of profit.

Now let’s move our focus to the Fed and its irredeemable dollar. The Fed exists to enable the government and favored cronies to borrow more, at lower interest, and without responsibility to extinguish their debts.

People often use the shorthand of saying that the Fed “prints” dollars. It is more accurate to say that it borrows them into existence, though there is no (knowing) lender. The Fed has the sole discretion to create these dollars ex nihilo, unlike a normal bank that must persuade a saver to deposit them. By this reason alone, the Fed’s credit is counterfeit. The very purpose of the Fed is to cause inflation, which I define as an expansion of counterfeit credit[1].

These borrowed dollars are the Fed’s liability. It uses them to buy assets such as bonds or to otherwise lend. Those bonds or loans are its assets. While the Fed can create its own funding, its own liabilities, it still must heed its balance sheet. If the value of its assets ever falls too far, the market will not accept its liability. Gold owners will refuse to bid on the dollar. Through a process of arbitrage (of course), the dollar will collapse.[2]

What does the government get from this game? It diverts resources away from value-creating activities into the government’s welfare programs, graft, regulatory agencies, and vast bureaucracy. By suppressing interest rates and enabling debts to be perpetually rolled, the Fed enables the government to consume much more than it could in a free market. Politicians are enabled to buy votes without raising taxes.

Earlier, I said there is no knowing lender. Let’s look at this mysterious unknowing lender. He is industrious and frugal, consuming less than he produces, keeping the difference as savings. He feeds this savings, the product of his hard work, into the government’s hungry maw. Unfortunately, the credit he extends is irredeemable. The paper promise he accepts has a warning written in fine print: it will never be honored. The lender is a self-sacrificial chump. Who is he?

He is anyone who has demand for dollars.

He is the trader who thinks that gold is “going up” (in terms of dollars). He is the businessman who uses the dollar as the unit of account on his income statement. He is the investor who measures his gains or losses in dollars. He is every enabler who does not distinguish between the dollar and money.

People don’t think of their savings in this light, that they are freely offering it to the government to consume. They don’t understand that savings is impossible using counterfeit credit.

Now we have covered the counterfeit credit of th Fed, let’s move on to cover another prerequisite topic: speculation. With arbitrage, I offered in Part II a much broader definition than the one commonly used. With speculation, I will now present a narrower concept than the usual definition. Let’s build up to it by looking at some examples.

The first example is the case of agricultural commodities, such as wheat. Production is subject to unpredictable conditions imposed by nature, like weather. If early rain reduces the wheat yield by 5%, then there could be a shortage. Think of the dislocations that would occur if the price of wheat remained low. Inventories from the prior crop would be consumed too rapidly at the old price. Then, when the reduced new crop was harvested, it would be too late for a small reduction in consumption. Grain consumers would suffer undue hardship.

Futures traders perform a valuable economic function. Their profit comes from helping to drive prices up (in this example) as soon as possible, and thus discourage consumption, encourage more production, and attract wheat to be shipped in from unaffected regions. Good traders study and anticipate nature-made risks to valuable goods and earn their profits by providing price signals to producers and consumers.

Trading commodities futures is a legitimate activity that helps people coordinate their activities. If such traders were removed, the result would be reduced coordination (i.e. waste). Therefore my definition of speculation excludes commodities traders.

There are two elephants in the room of the irredeemable currency regime: interest and foreign exchange rates. It is the profiteer in these games who earns the dubious label of speculator.

The price of each currency is constantly changing in terms of all others. To any business that operates across borders, this creates unbearable risk. They are forced to hedge. The banks that provide such hedging products must, themselves, hedge. One result is volatile currency markets.

The rate of interest presents the other big man-made risk. Unlike in gold, interest in irredeemable paper is always changing and is often quite volatile. For example, the interest rate on the 10-year Treasury bond has gone from 1.63% to 2.16% just during the month of May. As with currencies, there is a big need to hedge this risk, and hence, a massive derivatives market.

Naturally, volatility attracts traders, in this case the speculators. Their gains are not profits from anticipating natural risks to the production of real commodities. They are not skilled in responding to nature. They are front-runners of the artificial risks created by the next move of the government or central bank. Worse still, they seek to influence the government and central bank to act favorably to their interests.

Unlike the trader in commodities, the speculator in man-made irredeemable promises is a parasite. This is not a judgment of any particular speculator, but rather an indictment of the entire dollar regime. It imposes risks, losses, and costs on productive businesses, while transferring enormous gains to speculators.

It is no coincidence that the financial sector (and the derivatives market) has grown as the productive sector has been shrinking. A good analogy is to call it a cancer that consumes the economic body, by feeding on its capital. A free market does not offer gains to those who add no value, much less to parasites who consume value and destroy wealth. The rise of the speculator is due entirely to the perverse incentives created by coercive government interference.[3]

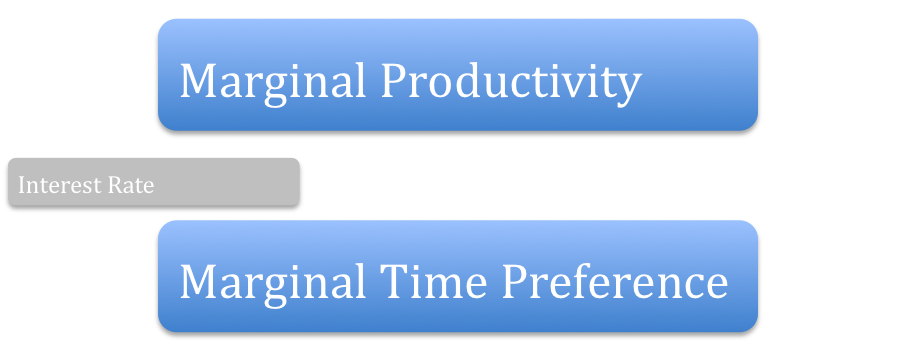

In light of the context we’ve established, we are now ready to start looking at interest rates. In the gold standard, the mechanism is fairly simple as I wrote in “The Unadulterated Gold Standard Part III (Features)”:

This trade-off between hoarding the gold coin and depositing it in the bank sets the floor under the rate of interest. Every depositor has his threshold. If the rate falls (or credit risk rises) sufficiently, and enough depositors at the margin withdraw their gold, then the banking system is deprived of deposits, which drives down the price of the bond which forces the rate of interest up. This is one half of the mechanism that acts to keep the rate of interest stable.

The ceiling above the interest rate is set by the marginal business. No business can borrow at a rate higher than its rate of profit. If the rate ticks above this, the marginal business is the first to buy back its outstanding bonds and sell capital stock (or at least not sell a bond to expand). Ultimately, the marginal businessman may liquidate and put his money into the bonds of a more productive enterprise.[4]

To state this in more abstract and precise terms, the rate of interest in the gold standard is always in a narrow range between marginal time preference and marginal productivity.[5]

The phenomena of time preference and productivity do not go away when there are legal tender laws. The government attempts to disenfranchise savers, to remove their influence over the rate of interest and their power to contract banking system credit.

In the gold standard, when one redeems a bank deposit or sells a bond, one takes home gold coins. This pushes up the rate of interest and forces a contraction of banking system credit. The reason to do this is because one does not like the rate of interest, or one is uncomfortable with the risk. It goes almost without saying that holding one’s savings in gold coins is preferable to lending with insufficient interest or excessive risk.

By contrast, in irredeemable currency, there is no real choice. A dollar bill is a zero yield credit. If one is forced to take the credit risk, then one might as well get some interest. Unlike gold, there is little reason to hoard dollar bills.

The central planners may impose their will on the market; it is within their power to distort the bond market. But they cannot repeal the law of gravity, increase the speed of light, or alter the nature of man. The laws of economics operate even under bad legislative law. There are horrible consequences to pushing the rate of interest below the marginal time preference, which we will study later in this series. The saver is not entirely disenfranchised. He can’t avoid harm, but his attempt to protect himself sets quite a dynamic in motion.

It should also be mentioned that speculators affect and are affected by the market for government credit. Their behavior is not random, nor scattered. Speculators often act as a herd, not being driven by arbitrage but by government policy. They anticipate and respond to volatility. They can often race from one side of a trade to the other, en masse. This is a good segue to our final prerequisite concept.

The linear Quantity Theory of Money tempts us to think that when the Fed pumps more dollars into the economy, this must cause prices to rise. If there were an analogous linear theory of airplane flight, it would predict that pulling back on the yoke under any circumstance would cause the plane to climb. Good pilots know that if the plane is descending in a spiral, pulling back will tighten the spiral. Many an inexperienced pilot has crashed from making this error.

The Fed adds another confounding factor: its pumping is not steady but pulsed. Both in the short- and the long-term, their dollar creation is not steady and smooth. Short term, they buy bonds on some days but not others. Long term, they sometimes pause to assess the results; they know there are leads and lags. They also provide verbal and non-verbal signals to attempt to influence the markets.

In a mechanical or electrical system, a periodic input of energy can cause oscillation. Antal Fekete first proposed that oscillation occurs in the monetary system. Here, he compares it to the collapse of an infamous bridge:

It is hyperdeflation [currently]. The Fed is desperately trying to fight it, but all is in vain. We are on a roller-coaster ride plunging the world into zero-velocity of money and into barter. In my lectures at the New Austrian School of Economics I often point out the similarity with the collapse of the Tacoma Bridge in 1941.[6]

I will end with a few questions. What happens if the central bank pushes the rate of interest below the marginal time preference? Could this set in motion a non-linear oscillation? If so, will this oscillation be damped via negative feedback akin to friction? Or will periodic inputs of credit inject positive feedback into the system, causing resonance?

In Part IV, we will answer these questions and, at last, dive in to the theory of prices and interest rates.

[3] See my dissertation for an extensive discussion of government interference: A Free Market for Goods, Services, and Money

[5] Interested readers are referred to the subsite on Professor Antal Fekete’s website where he presents his theory of interest and capital markets.

[6] Antal Fekete: Gold Backwardation and the Collapse of the Tacoma Bridge with Anthony Wile

I have a question regarding this statement: Savings is always finite, but the potential supply of bonds is unlimited.

In part I, you spoke about Statefulness, and then used the following example within the economy:

In the economy, a business that carries no debt will respond to a change in the rate of interest differently from one that is struggling to pay interest every month. A company which does not have cash flow problems but which has liabilities greater than its assets would react differently still.

My question is the following: since our current monetary system is a debt-based system (all money in existence is borrowed), couldn’t it be possible that the demand for credit, even the demand of potentially ALL entrepreneurs, falls to zero if the system becomes too loaded with liabilities?

I would like to hear your thoughts on this.

Thanks!

Paul,

Thanks for writing and I partially agree. Post-2008, there is reduced demand for credit for business growth. That said, it is a matter of how much the rate of interest falls. If it falls sufficiently, then it will cause capital churn. The next entrepreneur will borrow to buy capital to replace existing business capital (to the detriment of the latter). There is also demand by public companies to borrow to buy back their shares. And of course demand by most debtors to roll old liabilities with new, cheaper borrowing.

Got it. Thanks a lot. Your work is fantastic and I will be asking more questions as I continue to read.

Keith,

I have a comment/question regarding the below statement and whether one should be holding actual FRNs or Gold to protect against the bust that is coming. You state the following:

While the Fed can create its own funding, its own liabilities, it still must heed its balance sheet. If the value of its assets ever falls too far, the market will not accept its liability. Gold owners will refuse to bid on the dollar. Through a process of arbitrage (of course), the dollar will collapse.

Considering that the Fed must indeed heed its balance sheet, doesn’t this provide a natural “check” on the amount of currency that it can “print”? In a mature debt system, the likes of which most of the developed world has, isn’t a massive deflationary bust, where the current form of legal “money” (in our case FRNs) greatly rises in value while the overbearing debt burden deflates, the primary risk that people should be preparing for? Until laws are rewritten whereby the central bank or Treasury can literally create currency out of thin air (actually print as opposed to borrow it), isn’t the cash available to support all of the IOUs in existence naturally limited by the Fed’s balance sheet, thereby causing legal cash to be in the highest demand during the bust? If this is true, this would actually be a great reason to hoard dollar bills.

Thanks

Paul,

I wrote a short article called “Dollar Backwardation” which touches on some of the ideas raised by your question.

Holding is not to bet on its price (in dollars) rising, but rather that the Fed’s liability will be repudiated when its asset collapses. Look at India today. The market is questioning if it can keep paying on its bond, and so the rupee is falling like a rock.

Yep. That article answered it. “People could go on accepting paper dollars out of long habit” is, I think, the key sentence that I am looking for. It’s all about psychology. Once the psychology changes, the run on the dollar will commence. Thanks