Obamacare Imposes Perverse Incentives

Leave a reply

After markets closed on Friday, it was announced that Cyprus worked out a deal with the European Central Bank, European Commission, and the International Monetary Fund (“the Troika”). Here is a typical article reporting on the story.

Cyrpus has been in desperate need of a bailout, and was in discussions as early as June last year. They asked for an amount of money roughly equal to their annual GDP (for comparison, this would be about $15 trillion in the US!) The question is how did Cyprus arrive at this end of the road?

The root of the problem is the manufacture of counterfeit credit. Examples of counterfeit credit include Greek government bonds, sold by Greece to finance their social welfare state, Cyprus government bonds, sold by Cyprus to finance their social welfare state, and Cyprus bank debt, including deposits, used to finance the purchase of said Greek and Cyprus government bonds. To a bank, a deposit is a liability and it owns loans and bonds as assets.

As the world now knows, Greece is unable to pay. Greece is now mired in so-called “austerity”, a package-deal of falling government spending, rising tax rates, and no relief from crippling regulations. The result has been falling tax revenues, rising unemployment and social unrest. Holders of Greek government bonds (and Greek bank bonds) have taken losses already and will take more.

I define inflation as an expansion of counterfeit credit. Bond prices may rise for a time, making participants feel richer. But eventually, all debt borrowed without means or intent to repay is defaulted, and this is deflation. Default can come in many forms, and the imposed loss on depositors in Cyprus is no less a default than other forms. Deflation is now imploding in Cyprus.

In the initial proposal, depositors in Cyprus banks are to be stripped of 6.7% of deposits under €100,000 and 9.9% of amounts over that. Electronic bank transfers have been blocked and cash machines have run out of cash. A bank run is the inevitable reaction to the threat of loss of deposits in a bank.

Subsequent to the initial story, news is now coming out that the Cyprus parliament has postponed the decision and may in fact not be able to reach agreement. They may tinker with the percentages, to penalize smaller savers less (and larger savers more). However, the damage is already done. They have hit their savers with a grievous blow, and this will do irreparable harm to trust and confidence.

As well it should! In more civilized times, there was a long established precedent regarding the capital structure of a bank. Equity holders incur the first losses as they own the upside profits and capital gains. Next come unsecured creditors who are paid a higher interest rate, followed by secured bondholders who are paid a lower interest rate. Depositors are paid the lowest interest rate of all, but are assured to be made whole, even if it means every other class in the capital structure is utterly wiped out.

As caveat to the following paragraph, I acknowledge that I have not read anything definitive yet regarding bondholders. I present my assumptions (which I think are likely correct).

As with the bankruptcy of General Motors in the US, it looks like the rule of law and common sense has been recklessly set aside. The fruit from planting these bitter seeds will be harvested for many years hence. As with GM, political expediency drives pragmatic and ill-considered actions. In Cyprus, bondholders include politically connected banks and sovereign governments. Bureaucrats decided it would be acceptable to use depositors like sacrificial lambs. The only debate at the moment seems to be how to apportion the damage amongst “rich” and “non-rich” depositors.

In Part II (free registration required) we discuss the likely impact to the markets outside Cyprus, such as the euro, the dollar, gold and silver, and the US stock market.

When writing about economics (as opposed to trading), one does not expect to be proven right within days of publishing something. Things can take years to play out. On Monday, February 25, we published What Drives the Price of Gold and Silver? In that article, I wrote:

If there is a credible rumor that the Fed is planning to further extend its “Quantitative Easing”, how would you expect the monetary metals to react? Typically, the gold price would rise and the silver price would rise even more. The question is why.

Traders read the headlines and they know how the price “should” react to such news, and they begin buying. For a while, the prophecy fulfills itself. But then what happens next? It may take an hour or a month, but sooner or later some of the new buyers begin to sell. What can be bought on speculation using leverage must eventually be sold.

On Tuesday, Fed Chairman Bernanke testified before the Senate. Sure enough, the prices of gold and silver rose sharply. The next day, the prices were back down. By Thursday the price of silver was lower than it had been prior to his announcement.

On March 3, we published a video asking Is Bitcoin Money? While I appreciate many aspects of the cool technology behind it (being a software developer in a previous career), and noting that it has several features that uniquely suit it for certain markets, I concluded that it is an irredeemable currency, but not money (i.e. the most marketable commodity). I received much feedback on the video, some of it negative, though mostly thoughtful and engaging.

At the time of the video, Bitcoin was trading around under $40. Since then, it rose to about $48.

I was surprised to read that yesterday it fell to a low of $37. It has mostly recovered though it is now a few dollars below its high of $49. What happened?

The technical term is that the “blockchain forked”. In the video, I was very careful not to criticize the digital currency on technical grounds such its cryptographic technology, peer-to-peer networking, its data formats, methods of validating transactions, or communications over Internet Protocol, etc. I wanted to keep the discussion about monetary science. There is a point that I could have made, and will now make here.

If a currency is subject to Internet availability or other technological considerations, it simply is not money. It may still be useful for enabling commerce that would otherwise not be feasible—this is not an attack on Bitcoin as such. But (at least) one key characteristic of money is missing. Money must be beyond question by everyone and at all times. By nature, gold never becomes “unavailable” (though one could entrust it to an institution that suffers from unavailability of course).

When its “blockchain forked”, Bitcoin’s essence was called into question. Suddenly there were possible competing claims to the same coin, possible loss of coins, and certain lack of availability of the currency at least until engineers fixed the problem.

It has crashed before, too. On August 17, it moved from about $15.50 to $10.50 in a few hours. There were previous crashes before that, and there will likely be more (no this is not a prediction for next week!)

Technology aside, there is another factor that contributes to so-called “flash crashes”. If there is a wide bid-ask spread and/or the stack of bids is sparse, then it does not take much selling pressure to cause the price to collapse. For purposes of this discussion, let’s focus on the. While it is possible for the price to rise explosively, there is an important asymmetry between bid and ask: in times of extreme stress, it is always the bid that is withdrawn, never the ask.

Imagine if the US Geological Survey said that there would be a massive earthquake in Los Angeles, estimated to be 15 in the Richter Scale and which would not leave anything taller than a fire hydrant standing. There would be no lack of offers to sell real estate. What would be gone would be the bids. Anyone who needed to sell would have to accept peanuts, if he could even get that.

As I pen this, late Tuesday evening, I see a bid of $45.02 and an ask of $45.1377. This does not seem that bad, $0.1177 spread or about 26 basis points. But the bid looks thin to me! At $45.02, there is around 600 bid.

This is a screen capture I just took from Bitcoincharts.

With all the discussion on the Internet, some of it confusing, we thought a picture would be worth a thousand words.

Backwardation is when there is a profit to decarry the metal. This is the simultaneous sale of metal in the spot market and purchase of metal in the futures market. Selling is on the bid and buying is at the ask. So the spread one could earn is the decarry: Spot(bid) – Future(ask).

We normally quote this as an annualized percentage (the basis), but we thought we would show the raw numbers. This graph was made about 10:15am ET on March 4.

Sure enough, there is a 76-cent per ounce profit to be made decarrying gold. This is a small number compared to the price around $1600, and it could be easily missed. It is the actual profit one would make in the real market by this arbitrage (not including commissions and fees, which a bullion bank would not be paying).

It is fascinating that it persists. It’s been there for weeks! Does no one have gold to put towards this trade? Is there no attraction to a 0.3% annualized return on a risk-free trade maturing in less than 60 days?

Monetary Metals publishes the basis and cobasis with commentary every week (free registration required).

Far too many people believe that gold serves no useful purpose. I am therefore publishing this response to The 10 Minute Gold Standard: It’s Much Easier than You Think by Nathan Lewis. Mr. Lewis, a professed advocate of the gold standard, argues that even if we have a “gold standard”, we don’t need actual gold. Indeed, according to David Ricardo (quoted in the article), gold’s only job is to regulate the quantity of paper.

Mr. Lewis notes that when the Fed buys bonds it increases the quantity of dollars and when it sells bonds it decreases the quantity. This is true enough, but it’s not the quantity of dollars per se that is causing our ongoing capital crisis, or if you prefer, our solvency crisis. But I get ahead of myself.

The 10-Minute proposal is simple: the Fed should tweak its central planning. Instead of buying bonds to control the interest rate, it should buy bonds to control the gold price. However the unstated assumption, that the price of gold is based on the quantity of dollars, is false.

Gold is money, and paper (the dollar) is credit. The ratio of credit to money is not constant. Nor is the price of credit, which depends on its quality. Trying to control the gold price by this indirect proxy would be like trying to steer a car by opening and closing the windows.

The fatal flaw in the proposal is that paper cannot perform certain functions that can only be performed by gold. One is to extinguish debt. Paper currency is itself a credit instrument. The dollar is the liability of the Fed. Paying in paper transfers a debt, but the debt itself does not go out of existence. Since interest is constantly accruing, total debt rises exponentially.

Another function of gold that cannot be served by paper is hoarding. This is half of the key to understanding how interest rates are set in the real gold standard. A saver can withdraw his gold from the bank. This forces a contraction of credit and an increase in the rate of interest. In contrast, in a paper standard such as the “10 Minute Gold Standard”, there is no reason to sell a low-yielding bond in exchange for zero-yield dollar bill; the saver is disenfranchised.

Economists speak of “bond vigilantes” and assert that no one would buy a bond yielding less than the rate of “inflation”. In reality, the interest rate has been falling for 32 years. This long-term decline has done three things. It has continually lured in new borrowers, increased the burden of each dollar of debt, and caused incalculable destruction of capital.

The final stage of the Ponzi scheme of paper money is when debtors can’t pay the interest out of income. They must sell new bonds to pay off the old ones. The Fed is the enabler; its own bond purchases encourage speculators to front-run them. So long as the Treasury market holds up, the pretense can be maintained that the government is in good financial condition. Greece was the first of many countries to learn what happens when the bond market fails.

The world is rushing towards mass insolvency. If we don’t change course, we face certain devastation.

We urgently need the unadulterated gold standard. Those few of us who promote gold face a daunting task: to bring the message to the people and change course. I can understand the appeal of a quick fix that seems politically pragmatic, but the unworkable “10 Minute Gold Standard” only undermines gold standard advocates.

Postscript: Since this article is about money, readers may be interested in my latest video: Is Bitcoin Money?

If there is a credible rumor that the Fed is planning to further extend its “Quantitative Easing”, how would you expect the monetary metals to react? Typically, the gold price would rise and the silver price would rise even more. The question is why.

Traders read the headlines and they know how the price “should” react to such news, and they begin buying. For a while, the prophecy fulfills itself. But then what happens next? It may take an hour or a month, but sooner or later some of the new buyers begin to sell. What can be bought on speculation using leverage must eventually be sold. Traders who buy gold and silver futures think of their “profits” measured in dollars. They cannot profit from the rising gold price until they sell. So, sooner or later, they must sell. Alternatively, if the price goes down, they must sell because they are incurring losses at a multiple of the price drop due to their use of leverage.

Nearly all buyers of futures are speculators. They could be called “naked longs” because they have neither the intent nor the means to take delivery. Their predictable behavior when a particular contract heads into expiry has a characteristic behavior. One can see this in the gold and silver bases.

One way to debunk the “naked short seller” conspiracy theory is to watch the basis heading into First Notice Day. Naked longs must sell the expiring contract, and if they wish to remain long the metal, they must buy another farther-out contract. Right now, for example, we are in the late stages of “rolling” from the March silver contract to May (there were about 80,000 contracts open a month ago, and now about 30K).

Anyway, getting back to the topic, speculators are frequently driving up the price by buying news and rumors and almost as often driving down the price. In the short run, they can have an enormous impact on the price. But in the long run, they have almost none.

There are an estimated seven billion people on Earth. Most of them don’t read about the US stock market, the press releases from the Governor of the Bank of England, or the latest politics surrounding the appointment of a new head at the Bank of Japan. They don’t know how the price is supposed to move when earnings estimates for the S&P 500 are raised or lowered.

They are doing one of two things with physical metal. They are either slowly hoarding it, as the only safe store of wealth they can understand. Or they are performing arbitrage, each with his notion of the “right price”. When metal is priced lower than their threshold, these latter folks buy. When the price rises above, they sell. Most of them, of course, don’t even look at the price measured in dollars. They are using another currency, such as rupees.

The actions of the hoarders will sooner enough cause the final descent into permanent gold backwardation. But don’t count your paper “profits” just yet. This is not a time when gold owners get “rich”. Sure, the gold will have a high value indeed, though it may be worth your life to show anyone that you have it as occurred throughout history.

Permanent gold backwardation—the withdrawal of the gold bid on the dollar—will lead to bad times. Certainly, government policies are causing the capital base that supports our society to be hollowed out. If it can no longer support us, if the debt-based currencies no longer work, and if industries such as food distribution seize up due to lack of credit, then even the best case is pretty bleak.

For now, the actions of the arbitragers drive the price. Gold and silver are totally unlike any other commodities. Both metals have a stocks to flows ratio that is extraordinarily high. Stocks to flows is total global inventories divided by annual mine production. For gold and silver, this number is in the many decades. For other commodities, it’s measured in months.

All of this inventory is potential supply at the right price. If the price rises above the threshold set by a large number of owners, then metal comes into the market. If the price falls below this threshold (or the threshold ratchets up) then metal is taken out of the market.

The speculators can drive the price quite far in either direction, in the short term. But it is the hoarders and arbitrageurs who drive the price in the long term. A century ago, gold was worth about $20 an ounce. Now it is worth about $1600. This is another way of saying that the dollar has gone down to 1/80th its value. This trend is not going to end soon (or indeed end at all). But it does not move in a straight line, as these past few years have proven once again.

Wouldn’t it be nice to have an indicator that can help one determine whether hoarders and arbitrageurs are driving the price at the moment, or if it’s just the speculators again? This is precisely what the basis shows (among other things). In other words, are you buying your physical gold or silver into a speculative move (bad), or are your purchases part of fundamentals-driven move (good)?

Monetary Metals is now publishing graphs of the basis for gold and silver along with our commentary. Click here to view the Last Contango Basis Report (free registration required).

My series on the unadulterated gold standard was broken into five parts primarily to fit the format of The Gold Standard, the journal of Gold Standard Institute.

Here is the link to the GSI page that has them.

Communicating about money and finance in today’s culture is a real challenge; you want to inform and enlighten your audience on their level of knowledge—but this makes the use of terms extremely difficult. Ayn Rand Institute President Yaron Brook’s recent video about deflation demonstrates why.

In the video clip, Dr. Brook makes two key points. First, there is nothing bad about rising productivity and the consequence of falling prices. Second, there are no big credit collapses in a free market. I agree. These are important ideas that people need to hear, especially those receptive to free markets.

However, I have a concern regarding the word deflation.

When it comes to this type of communication—a presentation about a specific concept—clear thinking and precise language are essential. Using one word to describe both rising productivity in a free market and defaulting bad credit in a mixed economy does not advance our understanding of monetary science. Ayn Rand called this a package deal, which is basically taking two dissimilar things that have a superficial similarity and putting them into the same word.

Similarly, people often use the term inflation to mean rising prices, and then hold this up as the worst problem of the dollar system. Rising prices is not the main flaw with the dollar (it isn’t even in the top five list).

The root problem with the dollar is that it is irredeemable. It’s a promise to pay—a debt instrument—that can never be called, and will never be honored. Dollar-denominated debt can never be extinguished. Using a debt instrument to pay off a debt merely transfers the debt.

Let’s suppose that John owes money to Sue. So he pays her $1,000. John is now out of debt, but the debt does not disappear. The Federal Reserve now owes Sue $1,000. Next, she deposits it in a bank. Then the bank owes her and the Federal Reserve owes the bank. The lump can be moved around under the rug, but it’s still under the rug.

Every dollar was borrowed into existence. Borrowing always comes at interest. The catch is that, like all debts, accrued interest cannot be paid off. It is necessary to borrow more to make the payment.

This is why total debt must rise exponentially. What happens when the interest cannot be paid out of income? In the current phase, the debtor must sell new bonds to pay the interest and principal due on every bond as it matures. What happens when the last and biggest bond market, the U.S. Treasury bond market, fails? We don’t want to find out.

Taking a step back, we do not concede the definition of important concepts such as selfish to cater to a populist view. We point out that lying and stealing—which many wrongly describe as selfish—ultimately serve to destroy, not advance, one’s self-interest and are therefore selfless. Though genuine self-interest does include the desire for money, self-interest is about productiveness. Stealing is only superficially similar to being productive. Both are ostensibly undertaken to obtain money. But they are really opposites.

Similarly, the word deflation does not mean falling prices. As Dr. Brook explains in his video, there are at least two reasons why prices may fall; one is that productivity always rises in a free economy (and nothing needs to be done about rising productivity, as Dr. Brook notes). Another is when the central bank in a mixed economy forces a credit expansion, soon eough loans begin to default and credit contracts. These are two distinctly different phenomena that should not be bundled into one word.

I propose that inflation be defined as an expansion of counterfeit credit. Legitimate credit is when the saver is willing and the borrower has the means and intent to repay. If a loan is made when any of these elements is missing—which can only happen with the initiation of force or fraud—then what we have is counterfeit credit. Sooner or later, counterfeit credit always leads to defaults. I propose that the word deflation be used to denote forcible (i.e., involuntary) contraction of credit: a default.

By now, everyone should realize that the dollar is failing. Defining inflation and deflation in terms of issuance and default of bad loans makes the reason clear. Defining these terms as rising and falling prices confuses the issue.

This raises another, related issue. In the video, Dr. Brook says: “Today, you have this massive credit contraction … these deflationary pressures where money leaves the system, the amount of money in the system is contracting because banks on systemic scale are contracting the amount of loans that they are providing…”

This conflates money and credit. Testifying before Congress, J.P. Morgan famously said, “Money is gold, and nothing else.”1 Obviously, gold is neither created nor destroyed in the banking system.

Banks create credit. This is why banks exist. If loan defaults are rising, then banks are unable to expand credit and instead total credit in the system is contracting. This occurs whenever new loans are less than defaulted loans, which are written off. Credit, not money, is leaving the system.

Today, money is excluded from the system by law. The system is supposed to function on credit only. This makes it easy to confuse these different concepts and I think one could make a strong case that this confusion is deliberate.

The distinction between money and credit is not necessarily important to every discussion, but it is vitally important in a discussion of our monetary system. Credit cannot perform the job that must be done by money—to extinguish debt. Credit—especially counterfeit credit—can be created by the stroke of a pen and it can go out of existence when a debtor fails to pay for any reason.

We are fighting for nothing less than the survival of civilization. The irredeemable dollar is in the process of collapsing. If gold and silver do not begin circulating prior to the dollar’s terminal impact, we risk plunging into a new dark age. Our food production and distribution industries depend on credit, and deliver the goods just in time. A credit collapse could result in massive food shortages.

Many have tried and failed to promote the gold standard before now. There are a multitude of reasons why the gold standard has not been adopted, but the focus on prices is not a winning strategy to advance the cause of gold as money. Prices have been rising for decades. People accept this. Whether or not they are happy about it, they see no cause for alarm. We urgently need the gold standard, not because of rising prices, but because of an impending collapse of credit.

1 Testimony of J. P. Morgan before the Bank and Currency Committee of the House of Representatives, December 18 and 19, 1912. page 48

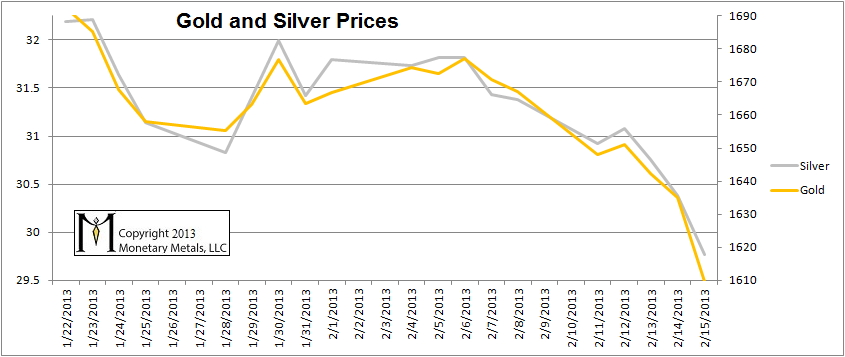

A curious thing happened last week. The prices of both monetary metals have been falling for a week and a half through February 15. No, that’s not the curious part. There is no law of nature that says the prices have to go up, but if they go down it must be artificial somehow. The curious thing is that the price fell while open interest in futures rose, which is not typical of how the market has actually been behaving in recent years.

Now let’s look at the data.

Silver loses about 6.6%, and gold about 4%; thus the gold:silver ratio gains about 2.6%.

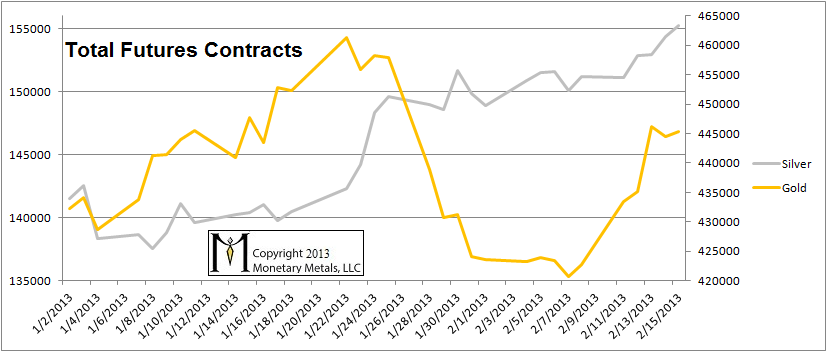

Next, let’s look at the open interest data, which is the number of futures contracts in each metal.

One possible explanation is the notorious “naked short sellers”. If so, they made money. Prices did fall. However, there is more data that doesn’t quite fit this theory.

As we showed, silver open interest was already quite high. It increased a few thousand contracts (under 2%) during the period through February 15. Gold open interest was not high by recent historical standards, and its open interest rose by 25,000 contracts (around 6%).

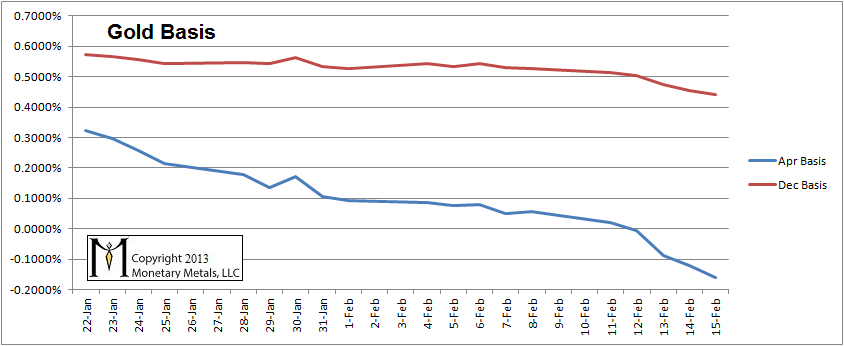

Now let’s look at the basis data (here is a short turtorial on the basis). This adds additional color to the data provided above.

The gold basis has been falling for a long time. The basis generally (but not always) moves in the opposite direction of the cobasis, and this linked article showed the cobasis rising. The falling gold basis is not news in itself.

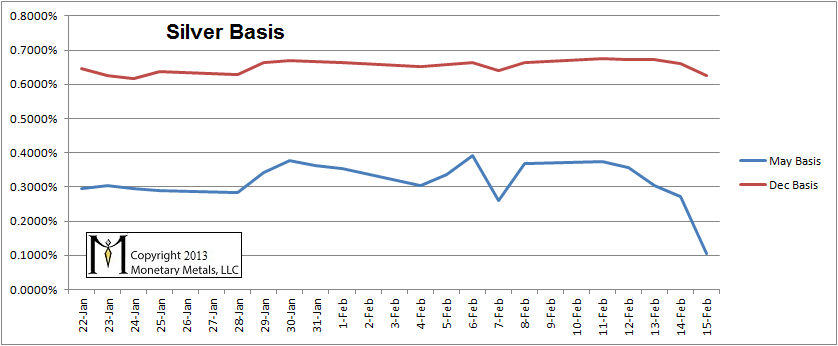

Let’s look at the silver basis.

In Part I, we looked at the period prior to and during the time of what we now call the Classical Gold Standard. It should be underscored that it worked pretty darned well. Under this standard, the United States produced more wealth at a faster pace than any other country before, or since. There were problems; such as laws to fix prices, and regulations to force banks to buy government bonds, but they were not an essential property of the gold standard.

In Part II, we went through the era of heavy-handed intrusion by governments all over the world, central planning by central banks, and some of the destructive consequences of their actions. We covered the destabilized interest rate, foreign exchange rates, the Triffin dilemma with an irredeemable paper reserve currency, and the inevitable gold default by the US government which occurred in 1971.

In Part III, we looked at the key features of the gold standard, emphasized the distinction between money (gold) and credit (everything else), and looked at bonds and the banking system including fractional reserves.

In Part IV, we discussed the problem of clearing. The problem of clearing arises when merchants deal in large gross amounts, on which they earn small net profits. They would not typically have the gold coin to pay for the gross value of the goods they purchase. This is an intractable problem in a strict gold-coin-only system and it only grows if specialized enterprises are added.

We considered the mechanics of Real Bills. It is interesting that goods flow from raw material producer to the consumer but the money flows from consumer to raw material producer. Without government involvement, and without banks, Real Bills circulate spontaneously.

In this final Part V, we look at the economics of Real Bills (or “Bills” for short). In Part IV, we noted that a Real Bill is credit that is not debt, so let’s start here.

The Real Bill is credit provided for clearing, without lending or borrowing. It is different than a bond. To review the bond, in Part III we showed how it arises out of the need to save. People must plan for retirement and senescence during their working years. Even if there is no way to lend at interest, this need still exists. So people hoarded part of their income by buying a commodity with a narrow bid-ask spread that was not perishable. Salt and silver are two commodities that were used for this purpose. For many reasons saving, in which one lends one’s wealth at interest, is superior to hoarding. Thus the bond was born.

The Real Bill is quite different. It isn’t lending at all. It is a clearing instrument that allows the goods to move to the gold-paying consumer before said consumer pays with gold. The Real Bill does not earn interest, and there are no monthly payments. The Real Bill is an opportunity to buy gold at a discount. The Real Bill sells in the market for less gold than its face value, based on the discount rate and the time to maturity. For example, a 1000g Bill would sell for 9975 grams 90 days from maturity, assuming the discount rate was 1%. When the merchant has sold all of the goods to consumers, and thus has all of the gold, he pays the bill with 1000g of gold.

By contrast, Bills occur wherever people consume. It is certain that people will eat bread tomorrow. Therefore, it is not risky to provide the gold to clear the flour sale. Bills come into existence because of the chronic need to consume. Bills increase in quantity at times of high seasonal consumer demand (such as Christmas) and decrease at times of low demand.

Bills provide the responsiveness necessary for a large and complex economy, without the sinister elements that come with “flexible” irredeemable paper money, central banking, and fiat elements such as “legal tender” laws. This is because Bills respond to market signals (the chief “virtue” of irredeemable paper money, or indeed any government interference in markets, is that does not). Most importantly, every Real Bill is extinguished after it has cleared one delivery of goods. Real Bills are said to be “self-liquidating”. Unlike the mortgage on a building, or the bond that finances a factory, the Real Bill is paid in full upon the sale of the asset it financed.

Real Bills are a simple mechanism, but they enable some very elegant arbitrages. For example, seasonal businesses have a problem for part of the year. What does the heating oil distributor do in the spring and summer? As he sells down his stocks of oil, he does not want to buy more oil. He can buy Bills, perhaps issued by a garden supply store that is in its busy season (and therefore is generating Bills). In this vignette, the heating oil distributor is directly financing the inventories of the garden supply! Without a bank or any other intermediary needed, it’s more efficient.

There is a subtler arbitrage, between retail merchandise and Real Bills. Every retailer can calculate a rate of return for every product on the shelves. The goods are financed by the issuance of Bills; it makes no sense to carry any goods that have a return lower than the discount rate. Instead, the retailer should not stock those goods and put spare capital into the Bills issued to finance higher-yielding merchandise. Today, without a market discount rate, even in the information age with software to track everything, many retailers make poor decisions of what merchandise to carry.

There are many other even more subtle arbitrages, but let’s look at one that is especially interesting. It is basic Econ 101 that if a natural disaster strikes then prices must rise. For example, if the wheat crop is hit by hail then there is a wheat shortage in the region. Prices must rise before wheat is diverted to the empty bakeries and hungry people. Real Bills provide a buffer mechanism. If the shortage is local (and hence small in proportion to the global market), what happens is that the discount rate falls in that region.

Let’s look at this. The Real Bill arises, as discussed above, from consumption. In case of shortage, there is greater confidence that goods shipped into the region will be consumed even more rapidly. A lower discount rate means that the distributor is effectively paid a higher amount. This will attract goods out of other regions where there is no shortage. It is not necessary for the baker to pay a higher price on flour, or for the consumer to pay a higher price for bread. What is necessary is that the distributor receives a higher price to divert the flour to the region. The lower discount rate provides that higher price.

Real Bills serve a vital role in the banking system, particularly for the savings bank. To back a demand deposit account, the bank can have 1/3 of the assets in gold and 2/3 in Real Bills. It must be emphasized that this has nothing to do with fractional reserves! The Real Bill is not lending. More importantly, the Bill market cannot go “no bid”. All Bills will be fully paid in 90 days, with the average being 45 days.

In contrast, with the lending of demand deposits (a form of duration mismatch), the system becomes unstable. This is not due to the risk of default per se. It is because the banks expand credit into a structure that is not in accord with the wishes of the savers. Eventually, it is guaranteed to collapse in a no-bid bond market with panic, liquidations, defaults, and bankruptcies.

The problem with duration mismatch is not merely one of liquidity. If today’s crisis, ongoing after more than four years(!) of flailing by central banks shows anything, it is that a mismatched and unbalanced credit structure cannot be fixed with liquidity. What happened is that projects for more and higher-order factors of production were started. But there was insufficient real capital to finance them, so those projects must be written offs with losses taken by banks and investors. The demand deposit backed by Bills does not create this problem.

In a free market, if people want a bank to provide only safe storage of gold with perhaps payment processing, then that service will exist for a fee. Such an account will effectively have a negative rate of interest. Most people prefer not to pay fees, and to earn a nominal rate of interest (in gold, of course there is no currency debasement so even 0.01% is positive). The Real Bill makes this possible.

Real Bills are a topic that could fill an entire book. The goal of parts IV and V iof this series is to provide an overview, show some of the elegant mechanisms of the Bills market, and address some of the controversy that has swirled around Real Bills from at least the time of Ludwig von Mises, and more recently when Professor Antal Fekete published his ideas about them on the Internet.

To conclude this entire series on the Unadulterated Gold Standard, it is fitting to provide the formal definition now that the reader has sufficient understanding of the concepts and ideas.

The unadulterated gold standard is a free market in money, credit, interest, and discount based on the right of the people to hold and use gold coins, and which includes Real Bills and bonds.

As we could only hint in this series, there are numerous specialists conducting transactions that are not obvious (or even counterintuitive) and the credit market can evolve into a structure that is quite complex. So long as there is no force or fraud involved, the system remains stable under a gold standard.